tiero/iStock via Getty Images

tiero/iStock via Getty Images

Granite Real Estate Investment Trust (GRP.U) (TSX:GRT.UN:CA) is a first-class operator of premium industrial and warehouse properties, offering a strong total return opportunity. With a track record of consecutive annual distribution increases averaging 4.5% over the past decade, Granite REIT has proven stability and boasts a best-in-class 99.1% occupancy ratio across its 128 warehouses and logistics properties.

Investment Thesis

Granite REIT's unique access to low-cost debt has allowed it to build a significant portfolio in some of the most important logistics hubs in North America and Europe. The company is well-positioned to benefit from strong tailwinds in the industrial space, including low availability and strong leasing demand. As Granite continues to diversify its portfolio and add scale in its largest markets, investors can expect to see NAV appreciation.

Company Profile

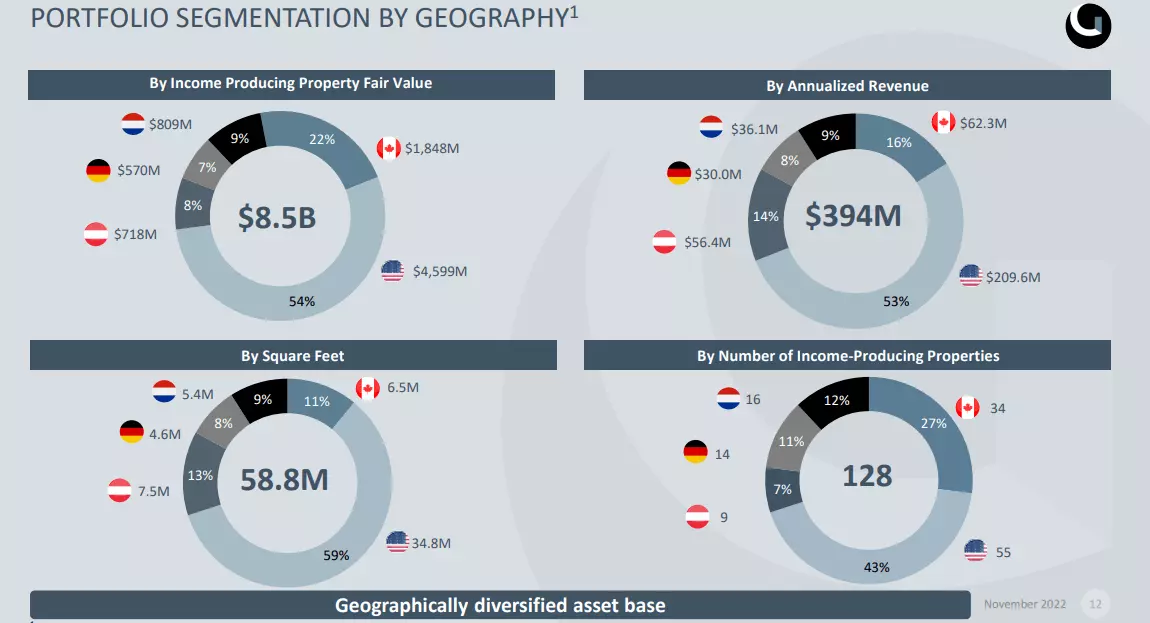

Granite REIT is an investment-grade REIT that owns and operates a portfolio of industrial properties in North America and Europe. Founded in 2003 as MI Developments Inc., the company has developed a substantial industrial real estate portfolio with interests in 141 investment properties encompassing 59 million square feet of GLA. The portfolio consists of e-commerce, distribution, warehouses, and logistics centers located in Canada, the United States, Germany, the Netherlands, and Austria.

Granite Operations Map (Granite REIT)

With a market cap of $5.3B and an enterprise value of $7.4B, Granite is the third-largest REIT by market cap listed in Canada. The company trades on both the S&P/TSX and NYSE under the symbols "GRT.UN" and "GRP.U," respectively.

Granite Portfolio Segment by Geography (Granite REIT)

Property Portfolio

Granite's portfolio consists of 88 e-commerce and distribution properties, accounting for 73% of the total portfolio. Additionally, the company owns 33 industrial/warehouse properties, seven special purpose properties, and three flex/office sites. With a remarkable 99.1% occupancy rate across its 128 income-producing properties, Granite's portfolio has a weighted average lease term of 5.7 years and an asset value of $8.9B.

Granite also holds 13 land and development sites, primarily concentrated in the U.S. Midwest and Southwest regions. These development sites provide opportunities for organic revenue growth and allow Granite to add scale in strategic locations. By focusing on major logistics hubs and transportation infrastructure in markets with strong demand, Granite has successfully pursued smaller expansion projects on existing sites with lower capital spends.

Magna Legacy

Granite's impressive achievement has been reducing its reliance on corporate sponsor Magna while achieving organic growth. Today, Magna accounts for 26% of annualized revenue, down from 45% in 2019 and over 95% at the IPO. This reduction was achieved through the disposition of Magna-leased properties and a robust development program, especially in e-commerce and distribution sites. While Magna remains an important client, Granite has successfully diversified its tenant base, with no tenant other than Magna accounting for more than 5% of annualized revenue.

Granite REIT Tenant Mix (Granite REIT)

Constructive Outlook for Industrials

Industrial REITs have demonstrated considerable resilience throughout the pandemic and post-pandemic periods. Industrial-focused REITs have maintained stable NAVs, unlike office and residential REITs. With low vacancy rates and strong leasing demand, the industrial sector is set up for continued success in 2023. The importance of logistics facilities has been underscored by post-pandemic supply chain challenges, leading retailers to invest in e-commerce capabilities. Strong demand for warehouses has resulted from reshoring activities and better inventory controls for firms with complex supply chains.

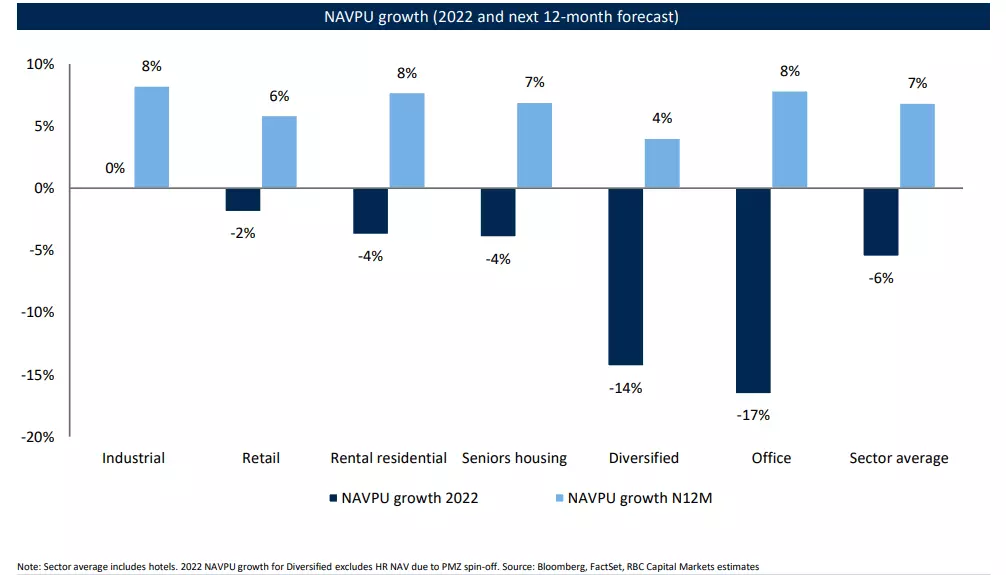

According to a report from RBC Capital Markets, industrial vacancy in Canada is at a record low of 1.5%, well below the 4.9% availability average since 2000. Limited new supply in 2023 and strong demand for high-quality industrial space will support strong revenue growth for Granite and other industrial-focused REITs.

Industrial REIT Outlook (RBC Capital Markets)

Industrial REIT Outlook (RBC Capital Markets)

Dividend Growth

Granite offers an annualized dividend of $3.20, paid in monthly distributions of $0.2667. With a current yield of 3.7%, slightly below its 5-year average yield of 4.1%, Granite has a 12-year dividend growth streak. The recent 3.2% increase in December 2022 is slightly below its 4-year annualized AFFO growth rate of 4.8%. However, Granite's 12 years of consecutive dividend increases make it the leading dividend growth REIT listed on the Toronto Stock Exchange.

Granite REIT Dividend Growth Rates (Author)

Granite's AFFO payout ratio is stable, with the most recent quarter at 80% and the last 12 months at 77%. Over the past 12 years of steady distribution increases, Granite has maintained a consistent FFO and a fairly consistent AFFO payout ratio. This stability and supported distribution growth, backed by growing free cash flow, provide investors with confidence in continued annual distribution increases.

Granite REIT Payout Ratio (Granite REIT)

Risk Analysis

Granite has a healthy balance sheet and best-in-class costs of capital. With total debt of $3.05B and liquidity of $1.27B, Granite has a healthy liquidity ratio of 42%. The company's weighted average effective interest rate is just 2.3%, compared to the industrial/office REIT subsector average of 3.2%.

Granite has a modest 30% net leverage ratio and a reasonable Debt/EBITDA ratio of 7X. Its Debt/EV ratio of 0.36, significantly lower than the Canadian average of 0.54, highlights a different capital structure. The company's debt is 98% fixed-rate with a weighted average term to maturity of 4.4 years. Along with SmartCentres REIT (SRU.UN:CA) (OTCPK:CWYUF) and Choice Properties REIT (OTC:PPRQF) (CHP.UN:CA), Granite holds a DBRS credit rating of BBB [HIGH]. Furthermore, with a cap rate of 4.9%, Granite is one of the few TSX-listed REITs with a sub-5% cap rate.

In March of 2022, DBRS Morningstar confirmed Granite REIT's senior unsecured debentures rating at BBB (HIGH) with stable trends, highlighting its institutional-quality industrial real estate portfolio, financial flexibility, strong lease profile, and unsecured debt capital stack.

Investor Takeaways

With a conservative balance sheet, stable business model supporting AFFO growth, and a constructive setup for industrial REITs in 2023, Granite REIT offers a great total return opportunity through NAV appreciation and distribution growth. As one of the highest-quality REITs on the S&P/TSX, Granite is an attractive investment option. Investors can have confidence in continued annual distribution increases and the long-term value creation of this logistics powerhouse.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.