Buying a home is a dream for many, but the idea of needing a large down payment can feel daunting. However, the truth is that homeownership is more accessible than you might think. In fact, there are options available today that allow you to buy a house with no money down.

Gone are the days of needing tens of thousands of dollars to become a homeowner. You don’t need a 20 percent down payment to buy a home. There are no money down mortgages probably available to you right now.

According to recent data, 38 percent of prospective buyers say that saving for a down payment is their biggest obstacle to homeownership. The average first-time buyer would spend nearly $25,000 on a down payment. But here's the good news: you can buy a house without that $25,000.

There are resources for down payment assistance that provide a clear path to homeownership. Some programs offer tax credits and grants to first-time buyers. And the best part? You don't have to wait for new federal legislation. You can buy a house with no money down today.

How to Buy a House With No Money Down

If you could live in your dream home for zero dollars down, would you still choose to rent? The reality is that you don't need a huge down payment to buy a home. First-time buyers typically put down an average of 7 percent.

But what about closing costs? That's where a no closing cost mortgage comes in handy. It raises your interest rate slightly, but allows you to keep money in your pocket.

Median Down Payment for First-Time Buyers

Median Down Payment for First-Time Buyers

There’s also down payment assistance available to help you get a mortgage with no money out of pocket. Federal, state, and non-profit agencies, as well as mortgage lenders, offer grants and loans to support first-time buyers.

1. Homebuyer Down Payment Assistance

Down payment assistance (DPA) programs can help you buy a home without immediate cash. These programs include federal, state, and non-profit options for first-time home buyers.

At Homebuyer, we partner with the Chenoa Fund to make homeownership possible without paying anything out of pocket. Through our partnerships, we provide DPA for buyers purchasing a home with an FHA loan, offering an affordable and user-friendly path to homeownership.

Buyers have two choices: a 3.5 percent second loan to cover your down payment, or a 5 percent second loan to cover down payment and closing costs. The best part is that the loan is forgivable if you make your housing payments on time.

The 3.5 percent option is forgiven after you make your first 36 mortgage payments on time, while the 5 percent option is forgiven after you make 10 years of payments without falling behind. There are also monthly payment options for higher-income earners.

These down payment assistance programs typically have credit history and income requirements, as well as the completion of a mortgage education course. The good news is that these options are available now.

2. USDA Loans With No Money Down

USDA loans are another option for buying a home with no money down. These loans have no down payment requirements and are designed to encourage increased homeownership in rural areas. The loans also provide subsidized interest rates.

To apply for a USDA loan, you need to prove creditworthiness and meet certain eligibility criteria, including being a legal permanent U.S. resident, maintaining dependable income, and having a household income below 115 percent of the area’s median income. USDA mortgages can be used to purchase existing homes, new construction, manufactured homes, condos, townhouses, and even short sale or foreclosed homes.

While buyers are typically responsible for closing costs, there are opportunities to have some expenses covered by the seller or your lender. Seller concessions and lender credits can help ease the financial burden.

3. VA Home Loans With No Down Payment

VA loans are specifically designed for U.S. military members, veterans, and their spouses. Like USDA loans, VA loans have no down payment or credit score requirements. However, most lenders prefer a credit score of 580 or higher.

To be eligible for a VA loan, you must have a certificate of eligibility (COE) that certifies your service history and current duty status.

The VA guarantees loans against losses with an entitlement, allowing lenders to offer a zero-down payment purchase with less risk and lower rates. VA loan borrowers are also exempt from certain closing costs, providing additional savings.

Qualifications by Loan Type:

| Minimum Credit Score | Minimum Down Payment | USDA Loans | VA Loans | FHA Loans | Conventional Loans |

|---|---|---|---|---|---|

| 580 | No Down Payment | Yes | Yes | Yes | Yes |

Conventional Loan 97 for First-Time Home Buyers

The Conventional Loan 97 from Fannie Mae allows borrowers to secure a conventional loan mortgage with a 3 percent down payment. Personal contribution isn’t required, as the down payment can be covered through mortgage gifts, grants, and other down payment assistance programs. The Conventional Loan 97 is an alternative to FHA loans, offering fewer upfront costs and no permanent mortgage insurance requirements. It is available to first-time home buyers who meet the eligibility criteria, such as having a fixed-rate interest mortgage on single-family homes up to four units, condos, and planned developments.

HomeReady Mortgages From Fannie Mae

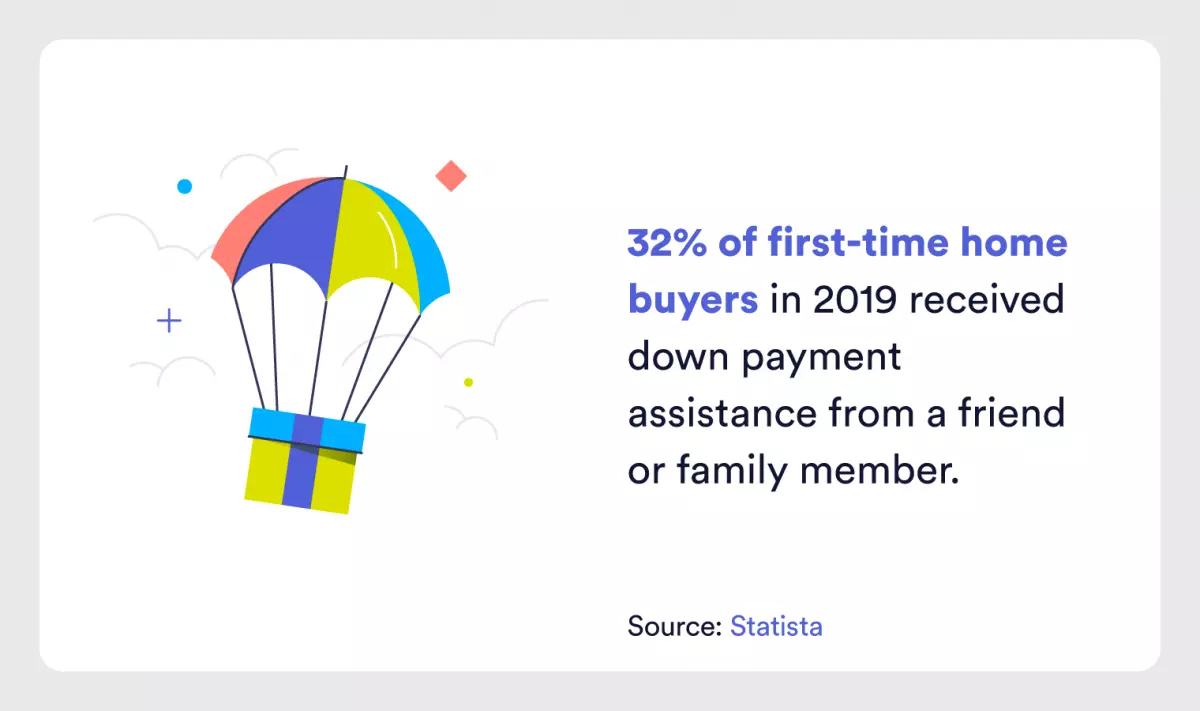

Graphic: 32 Percent Of First-Time Home Buyers Received Cash Gifts For Down Payment On A Home

HomeReady mortgages from Fannie Mae are another loan option for low-income buyers. Borrowers are eligible with a 3 percent down payment and a credit score of 620 or higher. Home buyer education is required for all first-time home buyers, and all residents' income can be considered for better chances of approval. There are no minimum personal contribution requirements for the down payment, as it can be covered by gifts, grants, and other down payment assistance programs. HomeReady loans require mortgage insurance that can be canceled once the buyer reaches 20 percent equity.

Freddie Mac Home Possible Mortgages

Freddie Mac’s Home Possible loans offer low down payment mortgages with a minimum 3 percent down payment. Down payment funding is flexible with no personal cash requirements. A credit score of 660 or higher is required for approval, and borrowers' income can't exceed 80 percent of the area median income (AMI). Home Possible mortgages may require mortgage insurance, which can be canceled once the buyer reaches 20 percent equity.

FHA Loans for Buyers With Low Credit Scores

FHA loans have a minimum 3.5 percent down payment requirement for borrowers with a credit score of 580 or higher. Borrowers with scores as low as 500 are eligible for approval if they invest a down payment of 10 percent or more. FHA loans also require proof of employment and income, as well as a debt-to-income ratio of 43 percent or less. FHA loans can only be used to purchase a primary residence, and county-specific loan limits apply. Get pre-approved to check your eligibility.

Conventional Loans With 3 Percent Down

Conventional loans are the most popular loan type among buyers. They require a minimum 3 percent down payment and a credit score of 620 or higher. Conventional loans also require mortgage insurance with a down payment under 20 percent. These loans aren't backed by the government, so lender requirements may vary. Conforming conventional loan limits follow FHFA standards, with the 2023 mortgage loan limit set at $726,200 for single-unit homes in most U.S. counties. Get pre-approved to check your eligibility.

Frequently Asked Questions

With the right loan type, many first-time home buyers can buy a house with no up-front costs. When you buy a house with no money down, you can lock in your housing payment long term, protect yourself from rent increases, and build wealth with a similar monthly payment as your rent.

Graphic: Rising Incomes Give First-Time Home Buyers More Purchasing Power As Compared To Last Decade

Graphic: Rising Incomes Give First-Time Home Buyers More Purchasing Power As Compared To Last Decade

What credit score do I need to buy a house?

You can buy a house with a credit score as low as 580, and sometimes even lower depending on your lender. VA and USDA loans have no official minimum, but lenders are likely to approve buyers with a credit score of 580 or higher. Conventional loans require a credit score of 620 or higher. You may still qualify for a loan with a credit score below 580. FHA loans accept credit scores as low as 500 if you can make a 10 percent or higher down payment.

Are there no down payment loans available?

Yes, there are options available for no down payment loans. In addition to down payment assistance programs, VA and USDA loans have no down payment requirements for qualification. Each loan type has other eligibility requirements for approval, such as military service for VA loans and rural property eligibility for USDA loans.

How can I save money for a down payment?

Down payment assistance programs help first-time and low-income buyers afford a home. Some loans accept down payments entirely funded through gifts, grants, and loans, so you may not have to contribute your own savings. Alternatively, create a comfortable budget and savings plan. Determine which loans you’re eligible for and their down payment requirements to set a goal. Consider how much you can save each month to determine your home-buying timeline.

Is private mortgage insurance (PMI) bad?

Mortgage insurance isn’t inherently bad. It helps protect lenders and allows them to offer low down payment mortgage options. Some loan types require PMI, while others may not. Homeowners pay PMI up-front, with an additional monthly payment, or a combination of the two. When considering mortgage insurance, think about the expense in relation to home prices, as waiting for a larger down payment may not be cost-effective in the long run.

Final Thoughts

Low and no down payment mortgages make homeownership accessible for first-time buyers. The key is to know which loans you’re eligible for and to get pre-approved for the mortgage of your choice. With the right information and guidance, you can navigate the path to affordable homeownership and make your dream of buying a house a reality.

Happy homebuying!