Benjamin Graham, the man who helped train Warren Buffett, suggested sticking to large companies to make investing easier. Although not a perfect solution, following his advice does help you avoid many pitfalls. If you're interested in dividends in general and real estate investment trusts (REITs) in particular, one giant name you should be looking at is Realty Income, which is about to get even bigger. Here's why you might want to add this net-lease leader to your portfolio today.

The Focus

Realty Income is what's known as a net-lease REIT. That means it owns properties, but its tenants are responsible for most of the costs of the assets they occupy. Although this is a vast simplification, Realty Income can just sit back and collect rent checks. This approach is generally considered to be fairly low risk.

With regard to the REIT's actual portfolio, roughly 84% of rents come from single-tenant retail properties, 11.5% from industrial, and 3% from office. The rest of the portfolio is in an opportunistic vineyard investment. About 7% of the company's rent roll comes from the United Kingdom. This investment provides a bit of geographic diversification as well as a toehold in Europe, a second region in which the company can look to expand.

The Size and Benefits Today

With a market capitalization of around $26 billion, Realty Income is one of the largest net-lease REITs in the industry. It operates a portfolio of nearly 6,600 properties. This provides important economies of scale since the REIT can leverage its employees over a large number of properties, which helps keep its operating costs relatively low.

Realty Income is also very careful with its balance sheet, which is investment-grade rated. That means when the REIT taps the bond market for cash, it will generally benefit from low interest rates. On the equity side, investors are aware of the company's long-term success (discussed in more detail below) and generally afford the stock a premium price compared to peers. That provides Realty Income with low equity capital costs, as well.

Cost advantages like these give Realty Income a huge head start when looking at acquisitions. And that advantage builds over time.

History of Success

There are a lot of different ways you can look at success, but when it comes to REITs one of the best is a company's dividend history. This is because REITs are specifically designed to pass income on to shareholders. On that front, this monthly-pay REIT has increased its dividend annually for 26 consecutive years, making it a Dividend Aristocrat. But that's not the end of the story; within that streak is a run of 94 consecutive quarterly increases.

To be fair, the average annualized dividend increase since Realty Income's 1994 IPO is around 4.4%, so this isn't a stock for people seeking swift growth. But for investors seeking out consistent dividend payers, it's hard to argue with the long-term success Realty Income has achieved. Note, too, that the quarterly and annual dividend streaks continued right through the coronavirus pandemic, which is an example of Realty Income's strength as a company.

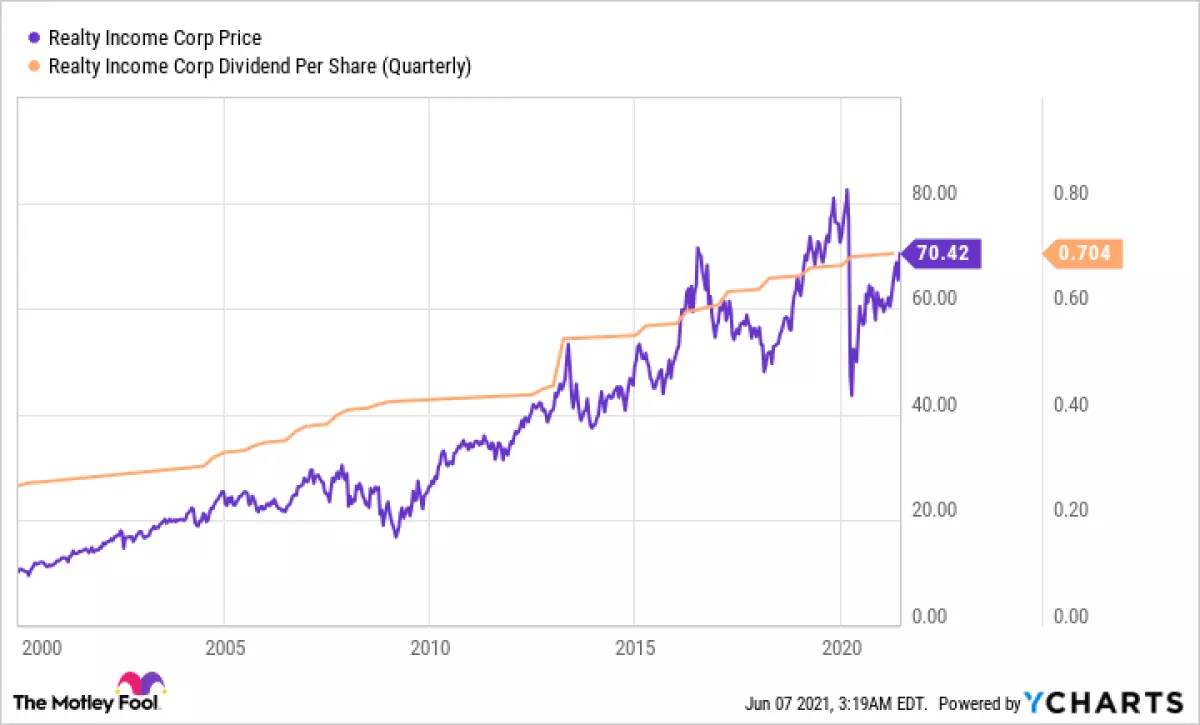

Realty Income's Performance

Realty Income's Performance

Getting Bigger

Realty Income's size recently allowed it to ink a deal to buy competitor VEREIT, another large net-lease REIT. When the deal is finally consummated, Realty Income's portfolio will expand to more than 10,000 properties and it will be the undisputed king of the net-lease sector. Its portfolio will remain roughly similar sector wise, though it currently plans to spin off its office assets into a separate REIT (office tends to be a more costly property type).

Realty Income expects the deal to be 10% accretive to adjusted funds from operations from the get-go. And, thanks to its high-quality balance sheet, it should be able to refinance VEREIT's debt over time at lower rates, creating even more of a financial advantage. As an even larger entity, Realty Income will be able to take on deals that others couldn't shoulder. The downside here is that its giant size will require more investment activity to foster growth, but with multiple markets to invest in and industry-leading access to capital, that shouldn't be too much of a headwind.

Time for a Deep Dive

If the idea of owning one of the largest and most reliable REITs on the market sounds like a good plan, then you should start looking at Realty Income. That said, its roughly 4% dividend yield isn't exactly huge and is in the middle-to-low end of its historical range over the past decade. So you are likely going to be paying full fare for this REIT today. However, paying a fair price for a great REIT that's about to get even better is probably worth it for more conservative investors. If you have a value bent, this is a name that you should keep on your wish list just in case there's a big market selloff.