Image source: JamesBrey

Image source: JamesBrey

Are you looking for an investment opportunity that offers a significant yield at a bargain price? Look no further than Rithm Capital (NYSE:RITM), a mortgage REIT that trades at an 18% discount to book value while presenting investors with a solid 10% yield. Despite its impressive value proposition, Rithm Capital remains underappreciated. In this article, we will explore the reasons why Rithm Capital is a hidden gem in the market and why it deserves your attention.

Rithm Capital has a diversified portfolio that generates significant, recurring earnings

Image source: Rithm Capital

Image source: Rithm Capital

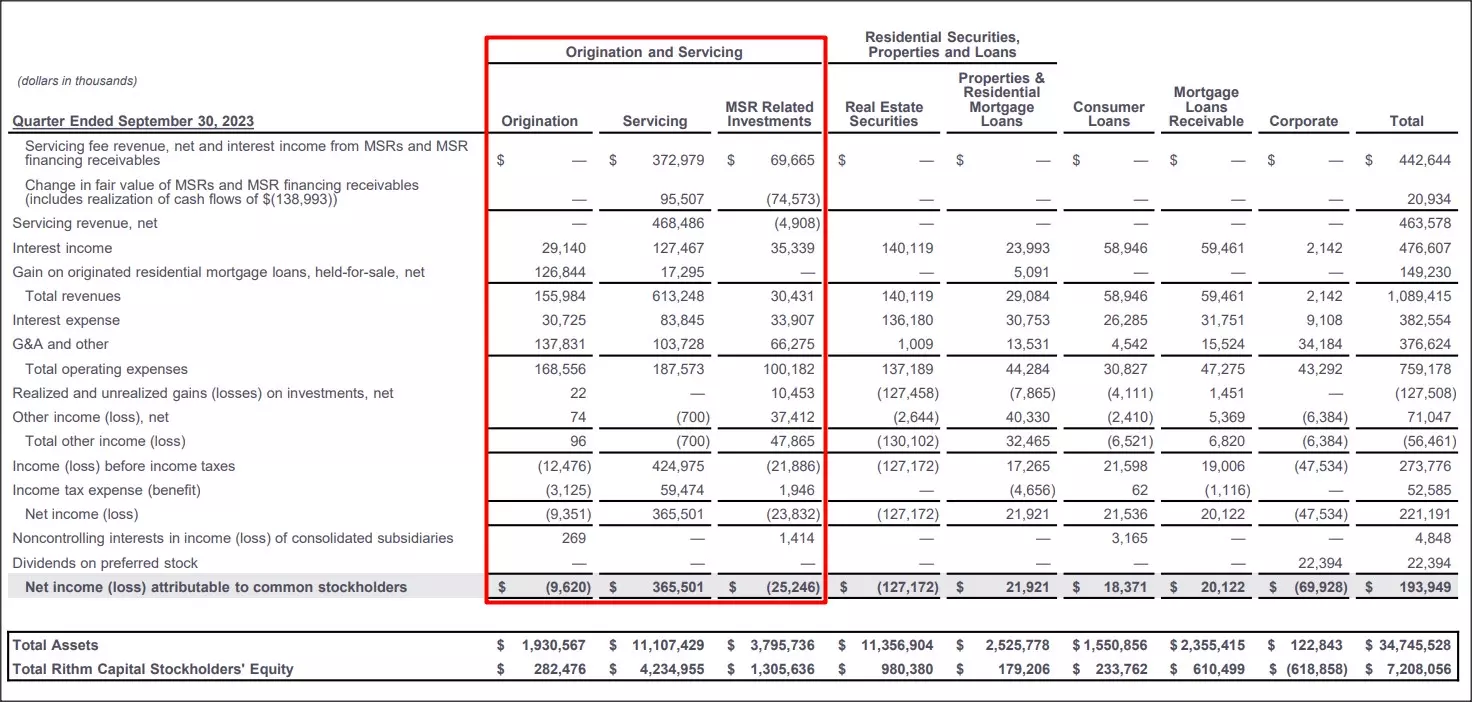

Rithm Capital sets itself apart from other mortgage REITs with its diverse investment portfolio. Unlike its counterparts, Rithm Capital invests in various sectors, including residential mortgage loans, mortgage servicing rights, rentals (single-family), consumer finance, commercial real estate, and servicer advances. This broad focus makes Rithm Capital one of the most diversified mortgage REITs in the industry.

The REIT's largest segment is origination and servicing, which generated substantial earnings of $330.6M in the third quarter alone. While Rithm Capital's other segments also contribute to its income, origination and servicing remain the primary drivers. However, it's worth noting that the REIT's business portfolio is rapidly evolving, as it continues to acquire new assets and businesses in the mortgage servicing and capital management segments. This strategic growth and diversification further strengthen Rithm Capital's revenue streams.

Rithm Capital offers a well-supported 10% dividend...

Rithm Capital's earnings power is evident in its coverage metrics. In the third quarter of 2023, the REIT posted $0.58 per share in earnings available for distribution (EAD). While there was a slight quarter-over-quarter decrease of 6% in earnings available for distribution, Rithm Capital's quarterly dividend of $0.25 per share remained well-supported. The EAD/dividend ratio for the third quarter was 232%, demonstrating the REIT's ability to cover its dividend payments effectively. In the first nine months of the year, Rithm Capital maintained an impressive EAD/dividend ratio of 207%.

Image source: Rithm Capital

Image source: Rithm Capital

Despite having the potential to raise its dividend, Rithm Capital has opted not to do so at the moment, as it focuses on pursuing business acquisitions. However, it's important to note that the REIT has managed to bring its dividend back to $0.25 per share after temporarily lowering it during the pandemic. This consistency in dividend payments reflects Rithm Capital's commitment to providing investors with attractive and reliable returns.

Why Rithm Capital is cheap

One might wonder why Rithm Capital's shares trade at an 18% discount to book value when the REIT boasts impressive dividend coverage. The reason for this significant discount lies in the unconventional nature of Rithm Capital's investment portfolio. The REIT's diverse mix of mortgage investments, including loans, mortgage servicing rights, and actual real estate, may make it more challenging for investors to fully grasp its potential compared to more straightforward mortgage REITs. Nonetheless, given the substantial support its earnings offer to its dividend, the current discount seems unwarranted.

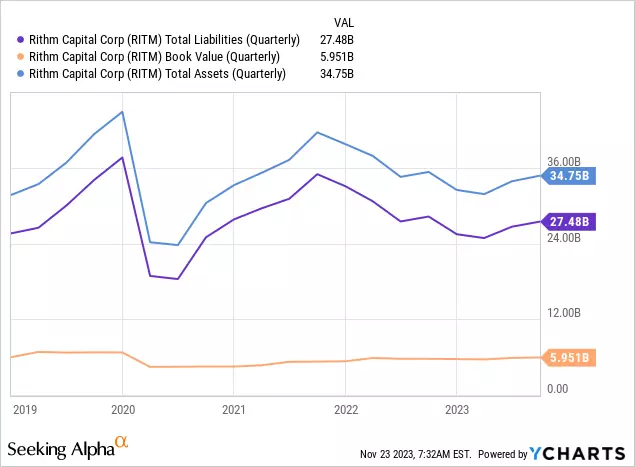

Chart source: Data by YCharts

Rithm Capital has traded at an average discount of 25% to book value over the past year, slightly above its current trading level. In comparison, other mortgage-focused investment companies like Annaly Capital and PennyMac Mortgage Investment trade closer to book value or at a lesser discount. While Rithm Capital's "more complex" portfolio composition may continue to result in a larger-than-usual discount, its potential for revaluation to book value is promising in the long term.

Risks with Rithm Capital

It's essential to consider the risks associated with investing in Rithm Capital. The persistent high discount to book value suggests that the gap may not narrow, as the market has long valued the REIT at a significant discount. However, investors primarily interested in Rithm Capital for its substantial and well-supported 10% dividend yield need not worry about this factor. Any concerns about Rithm Capital should arise if the margin between earnings available for distribution and the dividend narrows significantly or if the REIT starts trading at or above book value.

Final thoughts

While Rithm Capital's investment portfolio may seem more complex compared to other mortgage REITs, the core value it offers cannot be overlooked. With an excess coverage of over 200% based on earnings available for distribution in both the third quarter of 2023 and the first nine months of the year, Rithm Capital provides dividend investors with downside protection. Moreover, the magnificently covered 10% yield has the potential to grow further with higher distribution. Keep an eye on Rithm Capital as it continues to deliver value and generate attractive returns for investors.