Image Source: abadonian

Image Source: abadonian

Summary

Dream Industrial REIT (DIR.UN:CA / DREUF), a member of the Dream family of companies, manages a diverse portfolio of distribution, urban logistics, and light industrial assets across Canada, the US, and Europe. While initially appearing cheap, upon closer examination, DIR's valuation appears fair and lacks a substantial margin of safety. While we still believe in the industrial market fundamentals, we find Granite (GRP.UN) to be a more compelling option.

History

In the last few years, DIR has made significant acquisitions totaling over $4 billion, while also divesting non-core assets worth approximately $300 million. With a total return of around 28% in the past five years, DIR has outperformed the TSX Composite Index by 7 points and the TSX Capped REIT Index by 41 points.

In November '22, DIR formed a joint venture (JV) with GIC, the Singaporean Sovereign Wealth Fund, to acquire Summit Industrial Income REIT in a $5.9 billion all-cash deal. DIR holds a 10% stake in the JV, with GIC owning the remaining 90%. Acting as the JV's manager, DIR provides property management and other backend services. Despite its small contribution to DIR's overall portfolio, the JV has been active in property acquisition, development, and lease execution.

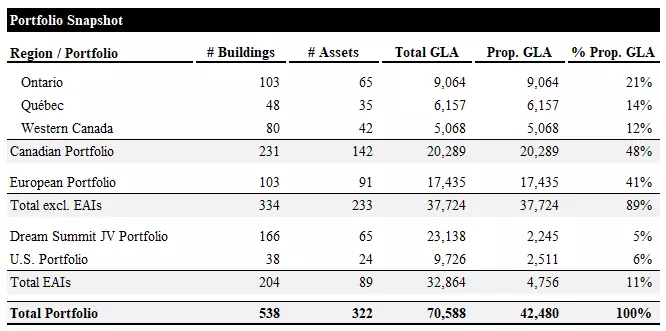

Portfolio Snapshot

DIR's owned portfolio consists of 233 properties, with approximately 37.7 million square feet of gross leaseable area (GLA), evenly split between Canada and Europe. Additionally, their Dream Summit and US JVs own 89 properties, totaling around 32.9 million square feet of GLA.

Image Source: Portfolio Snapshot (Empyrean; DIR)

The top ten tenants make up about 11% of gross recurring revenue and GLA. However, credit ratings are available for only two of these tenants, raising concerns about the overall creditworthiness of DIR's tenant base. This lower credit profile differentiates DIR from other major Canadian industrial REITs, like Granite.

Image Source: Top Tenants Summary (Empyrean; DIR)

Image Source: Top Tenants Summary (Empyrean; DIR)

While the composition of DIR's tenant base may not be a significant concern due to the nature of industrial assets, it does present an advantage for other industrial REITs, such as Granite.

Recent Performance

Earnings and Cash Flow Evolution

Examining DIR's earnings and cash flow from the end of '21 to Q3 '23, we observe several key drivers. DIR's Canadian portfolio experienced a 7% growth in GLA in Ontario and Quebec, with Western Canada remaining relatively flat. Ontario and Quebec boasted remarkable rent growth at approximately 15% and 12% CAGR, respectively, while Western Canada experienced modest growth of around 1% CAGR.

Image Source: Revenue Drivers: Canada (Empyrean; DIR)

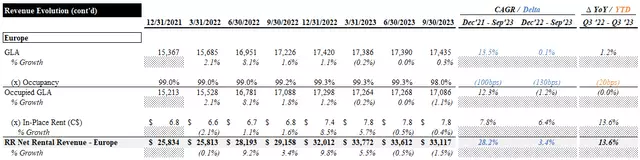

In Europe, DIR saw a 13% increase in GLA, with no significant change in occupancy. Rent grew at an approximate 8% CAGR.

Image Source: Revenue Drivers: Europe (Empyrean; DIR)

The US Fund experienced a 27% growth in GLA, with a slight decrease in occupancy. Rent also grew at a 5% CAGR. The Dream Summit JV, in its early stages, saw minimal changes in GLA, occupancy, and rent.

Image Source: Revenue Evolution: JVs (Empyrean; DIR)

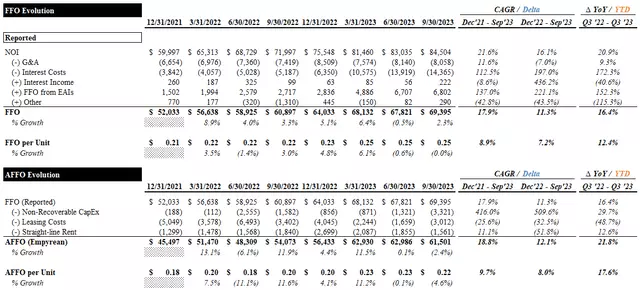

Reported rental revenue demonstrated a robust 20% CAGR, outpacing recoveries. Property management and other income increased eightfold, largely due to the contributions of the Summit JV. Operating expenses increased at a 16% CAGR, resulting in modest NOI margin expansion. Excluding property management and other income, NOI grew at a 19% CAGR, with NOI margins diluted by approximately 200 basis points.

Image Source: NOI Evolution (Empyrean; DIR)

FFO grew at an 18% CAGR, driven by positive operating leverage, FFO from equity accounted investments, and partially offset by significant growth in interest costs. AFFO, calculated by adjusting reported FFO for non-recoverable capex, leasing costs, and straight-line rent adjustments, grew at a 19% CAGR.

Image Source: FFO and AFFO Evolution (Empyrean; DIR)

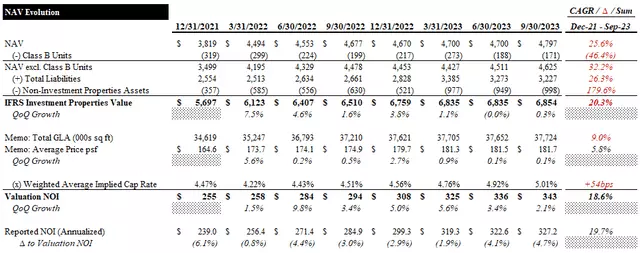

Payout ratios improved, with FFO and AFFO ratios aligning with Granite. DIR's reported NAVPU grew at a 6% CAGR, indicating growth despite unit issuances to fund acquisitions. However, this growth is only slightly higher than the price per square foot growth, leaving room for improvement. DIR's assets show potential for strong accretion due to attractive markets and significant loss-to-lease rent growth opportunities, but currently, Granite appears to have the advantage.

Valuation

Granite trades at 14.2x and 16.1x LQA FFO and AFFO, respectively, with FFO guidance for FY23 suggesting approximately 10% YoY growth. With an annual distribution of $0.70, Granite offers a yield of around 5%. Our NAV estimate reveals a slight discount in the market price, with an implied cap rate of approximately 5.3%.

Image Source: Valuation Summary (Empyrean; DIR)

Image Source: Valuation Summary (Empyrean; DIR)

Under our central case, DIR's target price reflects a 5% discount to NAVPU. This accounts for several factors, including a lower quality tenant base, higher European exposure, and the company's propensity for unit issuances. Even without the discount, DIR lacks a margin of safety. However, our upside case suggests a potential upside of approximately 7%.

Image Source: Target Prices (Empyrean; DIR)

While DIR's continued growth in the industrial market and loss-to-lease opportunities are favorable, it falls short of a strong recommendation. Instead, we recommend considering Granite for those seeking global industrial exposure through a Canadian REIT.

Risks / Catalysts

Despite a record level of new supply in Canada's industrial market, net leasing activity remains steady. Additionally, rising construction activity could soon converge with net absorption. Market rent growth in Canada continues to be positive, but the European market faces economic challenges that might dampen the growth potential for DIR's assets.

Image Source: Leasing Spreads (Empyrean; DIR)

Image Source: Leasing Spreads (Empyrean; DIR)

DIR's loss-to-lease opportunities remain significant, supporting strong revenue growth as leases expire. However, slower economic growth in Europe may pose challenges for realizing this potential.

Management Business

Property management income accounts for only about 3% of DIR's NOI, leading us to exclude it from our valuation. However, further growth in this income stream could provide additional upside to our target price.

Conclusion

While DIR may initially seem like a cost-effective way to enter the industrial market, a closer analysis reveals the pricing to be fair, rather than cheap. The lower quality of DIR's portfolio, significant European exposure, and reliance on equity-funded growth justify the discount in its valuation. While we maintain a positive outlook on the industrial market, we believe Granite offers a better opportunity.

Editor's Note: This article discusses securities that do not trade on major U.S. exchanges. Please be aware of the risks associated with these stocks.