Images courtesy of TennesseePhotographer/iStock via Getty Images and Data by YCharts

If you're on the hunt for a residential REIT with outstanding performance and promising potential, look no further than Dream Residential REIT (TSX:DRR.U:CA). This young REIT made a cool entrance into the market last year with its IPO and immediately caught our attention. With a solid management team, a low debt to asset ratio, attractive yields, and the potential for future growth, Dream Residential REIT stood out from its competitors. Yet, the market undervalued it, pricing it at just half its NAV. We saw an opportunity and made a strong recommendation.

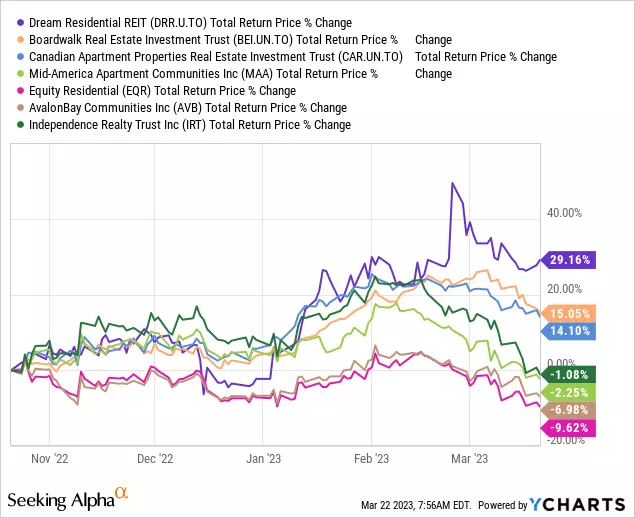

In our analysis, we stated, "If it even trades a bit higher from its current 12X AFFO to 14X AFFO or the cap rate gap closes, we get to a price of $8.40. That combined with its yield and the expectation of a reduction in cap rate, makes it a good buy for any portfolio." And we were right. Investors who took our advice and invested in Dream Residential REIT have seen impressive returns. It has outperformed not only its Canadian peers like Boardwalk REIT (BEI.UN:CA) and Canadian Apartment REIT (CAR.UN:CA), but it has also surpassed the US peer group. Equity Residential (EQR) lagged behind DRR by almost 39%, and AvalonBay Communities (AVB) fell short by 36%. Talk about outstanding performance!

Image: Suburban apartment complex

Image: Suburban apartment complex

Back in October, the market treated this newcomer harshly, assigning it an 8% implied capitalization rate [cap rate] compared to the REIT's calculated rate of 4.9%. However, with the release of Q4 results, DRR increased its weighted average cap rate to 5.22%, helping to dispel doubts about its value.

Despite the strong appreciation in its units, DRR still trades at an implied cap rate of close to 7%, making it an attractive investment opportunity. So, let's take a closer look at Dream Residential REIT to understand why it has been thriving in the market.

The REIT

DRR boasts a portfolio of 16 garden-style properties, comprising 3,432 units spread across the Sunbelt and Midwest regions of the US. These low-rise multifamily buildings offer residents access to ample green spaces, creating a comfortable and refreshing living environment.

Image: Garden-style properties from the 2022 Annual Report

Image: Garden-style properties from the 2022 Annual Report

Since its inception, DRR has consistently maintained high occupancy rates, consistently surpassing 90%. With an average term to maturity of 5.6 years, DRR is not burdened with refinancing until 2025. Moreover, its weighted average interest rate stands at 3.95%, enhancing its financial stability. As of December 31, 2022, DRR's debt to asset ratio was below 30%, and its interest coverage was 2.7X.

Investors in DRR enjoy a monthly distribution of $0.035 per unit, resulting in a current yield of 4.8%. Although this yield is lower than the 6% offered last October, it still remains competitive among its peers.

Q4 Results

DRR closed out 2022 on a positive note. It experienced a 1.8% increase in average monthly rent compared to the previous quarter, bringing occupancy levels up to an impressive 95.5%. Leasing spreads also saw a significant boost of over 8%. The REIT skillfully managed inflation effects, leading to slight expansion in net operating income (NOI) margins during the fourth quarter. The FFO for the year settled at $0.40 per unit. One of the highlights of the year was DRR's focus on property development. The REIT successfully completed 109 renovations across its properties during the quarter. Notably, these renovations resulted in a 30% increase in rents for the upgraded suites. Even non-renovated suites experienced a surge in demand, resulting in 15% higher expiring leases. Looking ahead, DRR plans to renovate approximately 400 more units in 2023, taking advantage of the positive outcomes yielded by previous renovations.

Valuation

Currently, DRR trades at an attractive multiple of around 13X FFO for 2023. In contrast, its peer group trades at a relatively expensive multiple of 18X. Dream Residential REIT's low multiple, coupled with its low debt, positions it as a rare gem in the residential space. Unlike its peers, DRR remains shielded from interest rate risks for the next two years. All things considered, with an implied cap rate of 7% and numerous other favorable qualities, DRR represents the best value within this sector.

Verdict

When it comes to choosing a residential REIT, DRR undoubtedly deserves your attention. While insider purchases have slowed down recently, one public market buy and the REIT's ongoing unit buyback program add confidence to the situation.

Image: Insider Ink

With approval to buy back close to a million units, DRR has already repurchased over 25,000 units as of February 23. These buybacks, combined with the successful execution of their plans, affirm the potential for an exceptional year ahead. Of course, it's essential to consider the inherent risk of a market meltdown, which could impact even the most promising investment. However, we believe that DRR merits attention despite this risk. Therefore, we maintain our buy rating with a $9.50 price target for 2023.

Please note that while this article provides valuable insights, it does not constitute financial advice. Investors should conduct their own due diligence and consult with professionals who understand their objectives and constraints.

Editor's Note: This article discusses securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.