Image source: Zephyr18

Image source: Zephyr18

Investment Thesis

Realty Income Corporation (NYSE:O) is a leading S&P 500 company and a member of the S&P 500 Dividend Aristocrats index. With a track record of consistently increasing dividends for over 25 years, Realty Income is a reliable investment option.

In my opinion, Realty Income has weathered the storm, and its current and projected dividend yield indicates a continued recovery rally until 2024. This thesis is supported by a favorable macroeconomic environment, attractive valuation, and strategic business development plans. If you already hold O stock, I recommend not closing out long positions. And if you're considering adding it to your long-term portfolio, now is still a good time to lock in the yield.

Why Do I Think So?

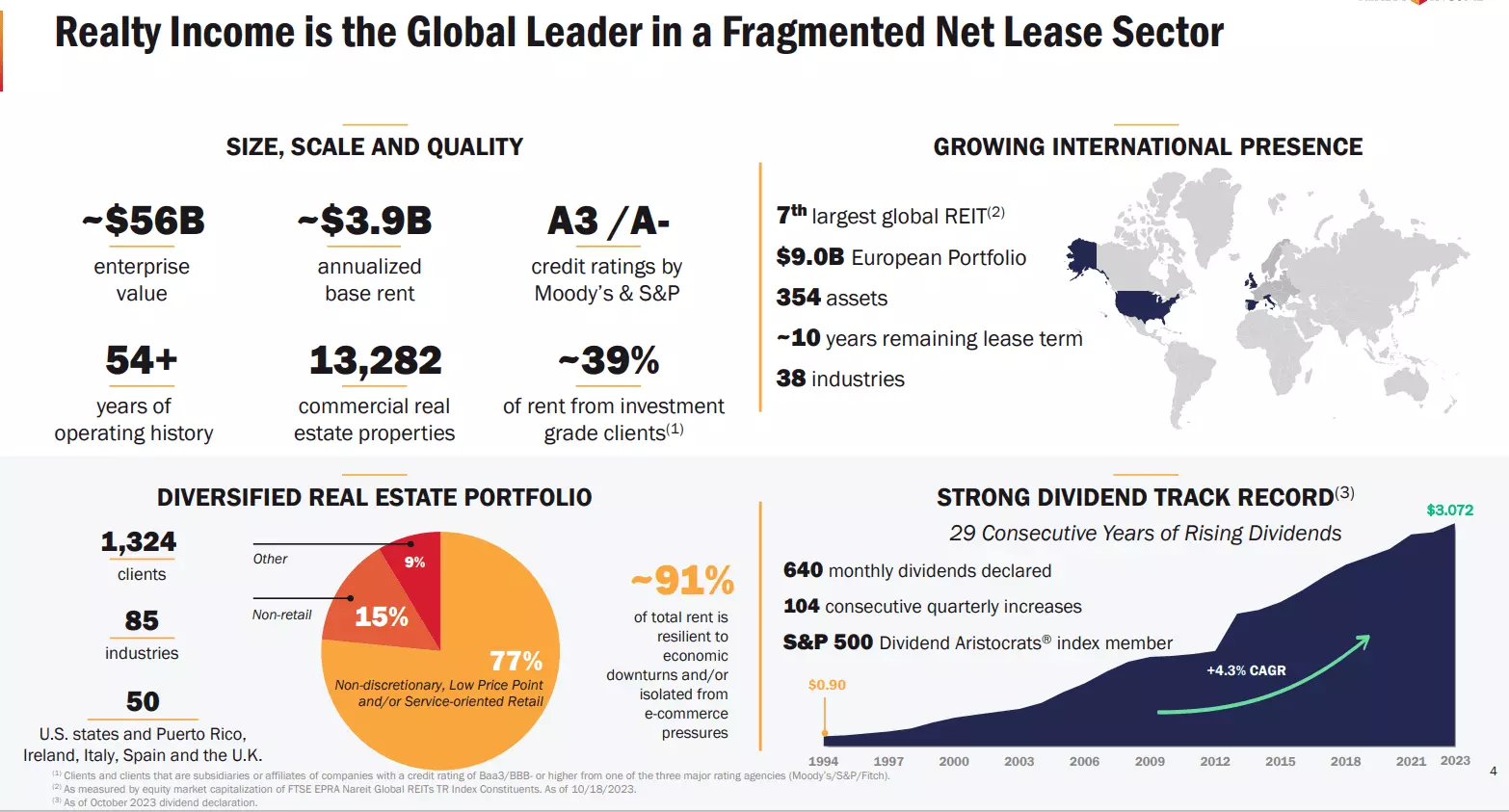

Operating as a real estate investment trust (REIT), Realty Income owns or holds interests in over 13,250 properties across various countries, totaling approximately 262.6 million square feet of leasable space. These properties are leased to commercial clients under long-term net lease agreements, ensuring a steady flow of monthly dividends. The company's diverse portfolio has a weighted average remaining lease term of approximately 9.7 years, with an annualized contractual rent of $3.87 billion. Moreover, about 39.0% of the annualized contractual rent originates from properties leased to investment-grade clients, which demonstrates the company's stability.

During Q3 FY2023, Realty Income showcased its financial resilience by investing $2 billion in high-quality acquisitions and raising over $2 billion in long-term and permanent capital. The company achieved a 2.2% same-store rental revenue growth and a rent recapture rate of 106.9% on re-leased properties. Realty Income's disciplined capital allocation approach, focusing on international markets, has contributed to its sustained growth. Despite challenging capital market conditions, the company achieved a 4.1% growth in Adjusted Funds from Operations (AFFO) per share, highlighting its commitment to consistent shareholder value creation.

Realty Income specializes in net lease retail, acquiring and owning single-tenant properties leased to strong national-brand retail chains under long-term contractual lease agreements. The company ended Q3 in a solid financial position with $4.5 billion in liquidity, and its net debt to annualized pro forma adjusted EBITDAre stood at 5.2x.

One significant event worth mentioning is the planned takeover of Spirit Realty Capital in a share swap worth $9.3 billion. This acquisition will significantly impact Realty Income's financial landscape and market position. It is expected to be more than 2.5% accretive to Realty Income's AFFO per share, with annual cost synergies of approximately $50 million. The acquisition enhances Realty Income's diversification, particularly in non-discretionary and service retail assets, solidifying its position as the fourth-largest REIT in the country.

Looking ahead, Realty Income remains cautious yet optimistic about capital allocation given the recent changes in the cost of capital. The company adjusted its investment guidance for 2023 to approximately $9 billion, excluding the Spirit transaction. The management emphasizes a highly selective approach to pursuing new opportunities, focusing on generating ample spreads to its cost of capital. With a healthy portfolio performance, strong financial discipline, and the pending merger with Spirit Realty, Realty Income is positioned favorably for continued stability and growth in the real estate investment landscape.

Image source: O's IR materials

In my opinion, for Realty Income to continue its development, it needs a change in market sentiment and a softer macro environment for REITs. Fortunately, recent weeks have shown positive signs of fulfilling this need.

The Market Gives an Opportunity

According to Bank of America's analysts, the Real Estate sector in FY2024 appears to be a "diamond in the rough," offering attractive income options. About 30% of the sector's constituents now offer yields higher than the 10-year yield, making them appealing choices for investors.

The anticipated monetary policy paradigm shift, expected as early as 2024, presents an even more favorable scenario for REITs. Real estate stocks today behave differently compared to similar periods in past economic cycles, indicating that the potential for a positive reaction to the upcoming monetary policy turnaround is not yet fully embedded in their prices.

Key Bank analysts also support the positive outlook for retail REITs, with strong leasing demand, a significant leasing backlog, and robust renewal rent spreads contributing to above-trend growth in 2024 and 2025. Despite potential challenges from consumer weakness, Realty Income's competitive advantage of high-quality diversification positions the company to withstand headwinds of this nature.

It's essential to note that Realty Income's specialization as a net lease retail REIT brings stability and protection during economic downturns. With long leases, strong tenants, and a focus on essential goods and services, the company maintains high occupancy rates and consistent revenue generation. While potential drawbacks include limited growth potential in the mature and competitive net lease retail market, challenges in expansion, and sensitivity to rising interest rates, these factors have already been reflected in the O stock price.

![BofA [December 2023]](https://sanaulac.vn/uploads/images/blog/admin/2024/01/23/realty-income-expect-solid-total-returns-in-2024-1705990714.webp) Image source: BofA [December 2023]

Image source: BofA [December 2023]

Realty's Valuation Analysis

As with any REIT, Realty Income is sensitive to changes in interest rates. With the market factoring in the peak in the fed funds rate, the stock price experienced a rapid rise, interrupting the growth of the dividend yield.

Considering the historical average dividend yield over the last 10 years, O's dividend yield should fall further following the principle of mean reversion.

However, the current macro regime, which suggests maintaining high interest rates for longer due to a strong labor market and potential inflation risks, may challenge the correlation between dividend yield and interest rates.

Another valuation metric, EV/EBITDA ratios, is expected to decline sharply next year due to predicted rapid EBITDA growth. This sizable decline seems disproportionate to the growth, raising questions about fairness.

Image source: YCharts, author's notes

The growing discount to EV/EBITDA can be attributed to the increase in leverage in recent quarters. However, as EBITDA rises, it is reasonable to expect O stocks to return to the lower end of their historical EV/EBITDA range, which is around 16x. With a forecasted EBITDA of $4.83 billion, I estimate a fair equity value of approximately $56.7 billion after adjusting for net debt. This indicates an upside potential of 32.2%, without considering the dividend yield of over 5%.

A more classic metric, the price-to-FFO ratio, confirms the conclusion above. The O stock's price-to-FFO ratio of ~12x is currently below its long-term average of 16-17x, suggesting an upside potential of around 37.5% to reach the mean.

Image source: YCharts, author's notes

Image source: YCharts, author's notes

The Bottom Line

The main risk associated with Realty Income is its growing credit risk, despite the structured acquisition of Spirit Realty Capital. The increase in liabilities on the consolidated company's balance sheet may impact the company's risk profile and potentially widen the discount in O's valuation. Economic downturns can also affect tenant stability and rental income. Therefore, careful evaluation of tenant risk is crucial to assess Realty Income's performance.

However, despite these risks, I remain confident in Realty Income Corporation's growth potential in the medium term. By the end of 2024, I expect the O stock to return to a sub-5% dividend rate due to rate cuts by the Fed and mean reversion in valuation multiples. If my predictions hold true, investors can anticipate a total return of over 30%, making O stock a compelling "Buy" today.

Thank you for reading!